EUR/USD is lower in Thursday’s European session, as the pair has dipped below the 1.28 line. The markets are waiting for the ECB interest rate announcement and comments by Mario Draghi, the head of the ECB. In other economic news, Spanish and Italian Services PMIs rose slightly, but remain below the 50-point level, which indicates expansion. Spain also conducted a 10-year bond auction, which posted a lower yield than the previous auction. In the US, today’s key release is Unemployment Claims. As well, US Federal Reserve head Bernard Bernanke will address an education conference in Dayton, Ohio.

-->

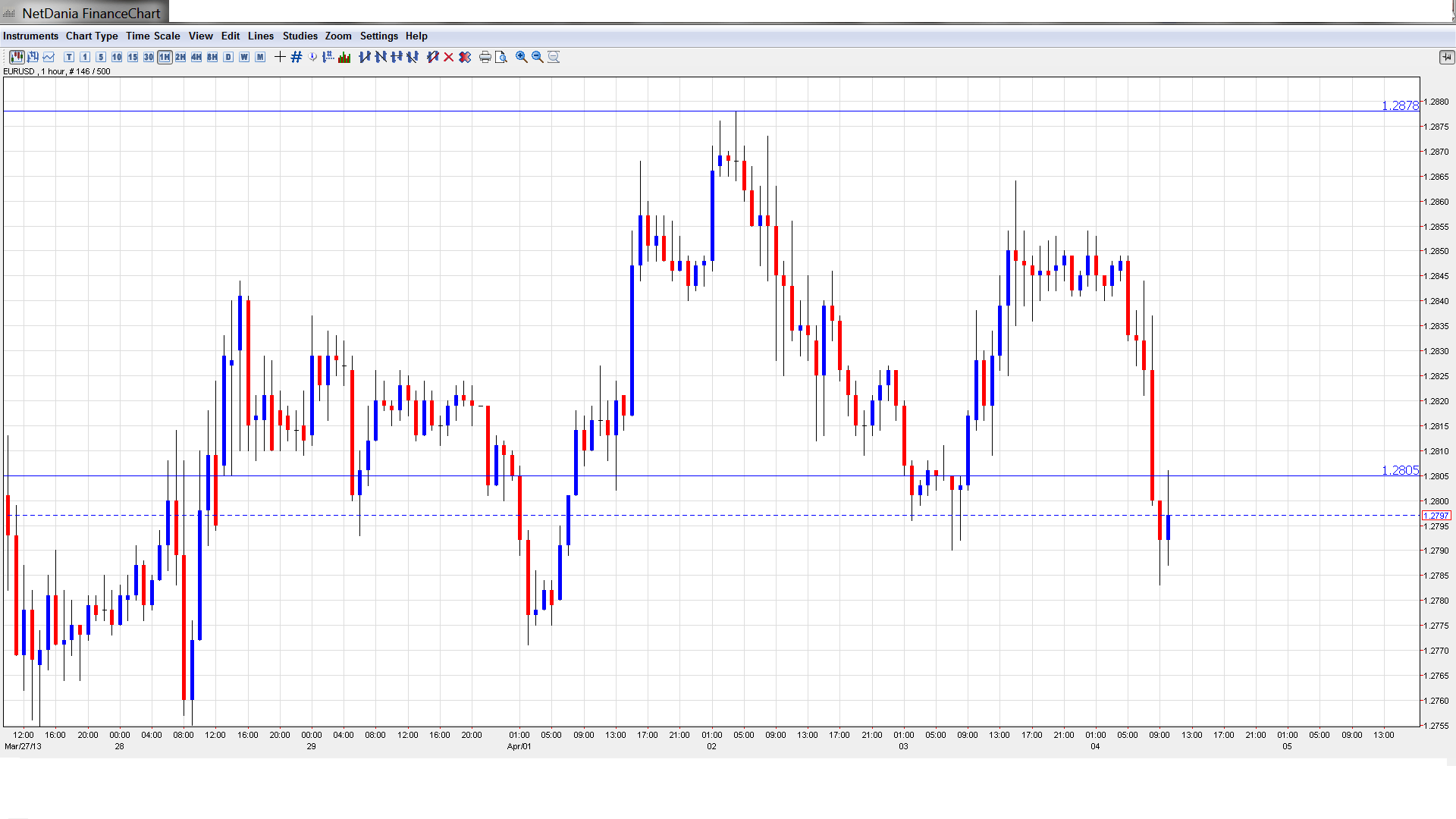

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

EUR/USD Technical

- Asian session: Euro/dollar was steady, touching a high of 1.2828 and consolidating at 1.2835. The pair has weakened in the European session, dipping below the 1.28 line.

- Current range: 1.2746 to 1.2805

Further levels in both directions:

- Below: 1.2746, 1.27, 1.2660 and 1.2587.

- Above: 1.2805, 1.2880, 1.2960, 1.3000, 1.3100, 1.3130 and 1.3170.

- 1.2746 is the next support level.

- 1.2805 is providing weak resistance. 1.2880 is stronger.

Euro dips below 1.28 ahead of ECB meeting– click on the graph to enlarge.

EUR/USD Fundamentals

- 7:15 Spanish Services PMI. Exp. 44.3 points. Actual 45.3 points.

- 7:45 Italian Services PMI. Exp. 43.4 points. Actual 45.5 points.

- 8:00 Eurozone Final Services PMI. Exp. 46.5 points. Actual 46.4 points.

- 8:45 Spanish 10-year Bond Auction. Actual 4.48%.

- 9:00 Eurozone PPI. Exp. 0.2%. Actual 0.2%.

- 9:02 French 10-year Bond Auction. Actual 1.94%.

- 11:30 US Challenger Job Cuts.

- 11:45 ECB Minimum Bid Rate. Exp. 0.75%.

- 12:30 ECB Press Conference.

- 12:30 US Unemployment Claims. Exp. 352K.

- 12:45 US FOMC Member Charles Evan Speaks.

- 14:30 US Fed Chairman Bernard Bernanke Speaks.

- 14:30 US Natural Gas Storage. Exp. -89B.

- 16:30 US FOMC Member Esther George Speaks.

- 21:00 US FOMC Member Janet Yellen Speaks.

For more events and lines, see the Euro to dollar forecast

EUR/USD Sentiment

- Markets anxious before ECB meeting: In what has become somewhat of a routine, the markets are not paying much attention to the ECB interest rate announcement, as rates are widely expected to remain at the current level of 0.75%. What has instead become a market-mover is the follow-up press conference hosted by ECB head Mario Draghi. This time, Draghi will not be able to get away with repeating that he is fully confident that the ECB economy will improve sometime during the year. The Cyprus bailout rocked financial markets and has taken a toll on investor confidence, leaving the markets jittery. With Eurozone releases pointing to a deterioration in the economy, Draghi will be hard pressed to calm the markets.

- Cyprus deposits face huge hit: The bailout agreement may have been signed, but the drama and uncertainty surrounding the Cyprus bailout plan continue. Capital controls are still in place in Cyprus, as the government remains fearful of a run on the banks. Over the weekend, authorities revealed the plan for taxing around 60% of the money on big accounts (above 100K) in the Bank of Cyprus. This steep tax is expected to have a strong negative impact on the country’s business sector, and the government has admitted that the country is in recession. In order to help the slumping economy, Cyprus plans to lift a ban on casinos and provide tax exemptions on business profits that are reinvested on the island. President Nicos Anastasiades has acknowledged that the bailout agreement is painful for Cypriots, but said that failure to reach a deal would have resulted in the collapse of the banking sector and could have led to an exit from the Eurozone. Meanwhile, Cyprus finance minister Michael Sarris has resigned. Sarris said he had done so in order to facilitate a formal investigation, which will examine the events leading up to the 10 billion euro bailout.

- Eurozone PMIs falter: There has been talk of the Eurozone economy improving sometime in 2013, but so far this year, the economy has not shown much in the way of a recovery. This has been underscored by disappointing data this week. PMI numbers out of Spain, Italy and the Eurozone point to continuing contraction in the services and manufacturing sectors, with consistent readings below the 50-point level. Meanwhile, the employment situation on the continent is a disaster, as the Unemployment Rate in the Eurozone edged up to a record high of 12.0%. The euro has responded by losing ground, and will likely dip further is we don’t see better numbers out of the Eurozone.

- Italian political impasse continues: After coalition talks failed, the Italian president reportedly considered resigning in order to accelerate the path to fresh elections. However, and perhaps due to pressure from ECB president Mario Draghi, President Napolitano instead appointed a panel of 10 experts, including politicians and a member of the country’s central bank, in order to try and find another political solution. The Italian media has playfully dubbed the panel the “Ten Wise Men”. All humor aside, these “wise men” will have their hands full trying to untie the Gordian knot of the inconclusive election results, which has left the Eurozone’s third largest economy in a deep political crisis. Also Italy’s small neighbor, Slovenia, has some issues. Here is some background about Slovenia.

- US data points downward: Last week saw a host of dismal US releases, as manufacturing, housing, consumer confidence and employment figures were all weak. The month of April has not brught any relief, as PMI numbers and the ADP Non-Farm Payrolls fell way below expectations. Further weak numbers are likely to raise red flags about the health of the US economy.

0 comments :

Post a Comment