continues where it ended last week, trading in the mid-1.29 range. The week ended on a high note, as both US and German numbers beat expectations. GfK German Consumer Climate posted a multi-year high, and German Ifo Business Climate easily beat the estimate. In the US , Core Durable Goods Orders bounced back and recorded a strong gain. Monday will be marked by thin volume, as the US markets are closed for a holiday, and there are no releases out of the Eurozone.

continues where it ended last week, trading in the mid-1.29 range. The week ended on a high note, as both US and German numbers beat expectations. GfK German Consumer Climate posted a multi-year high, and German Ifo Business Climate easily beat the estimate. In the US , Core Durable Goods Orders bounced back and recorded a strong gain. Monday will be marked by thin volume, as the US markets are closed for a holiday, and there are no releases out of the Eurozone.

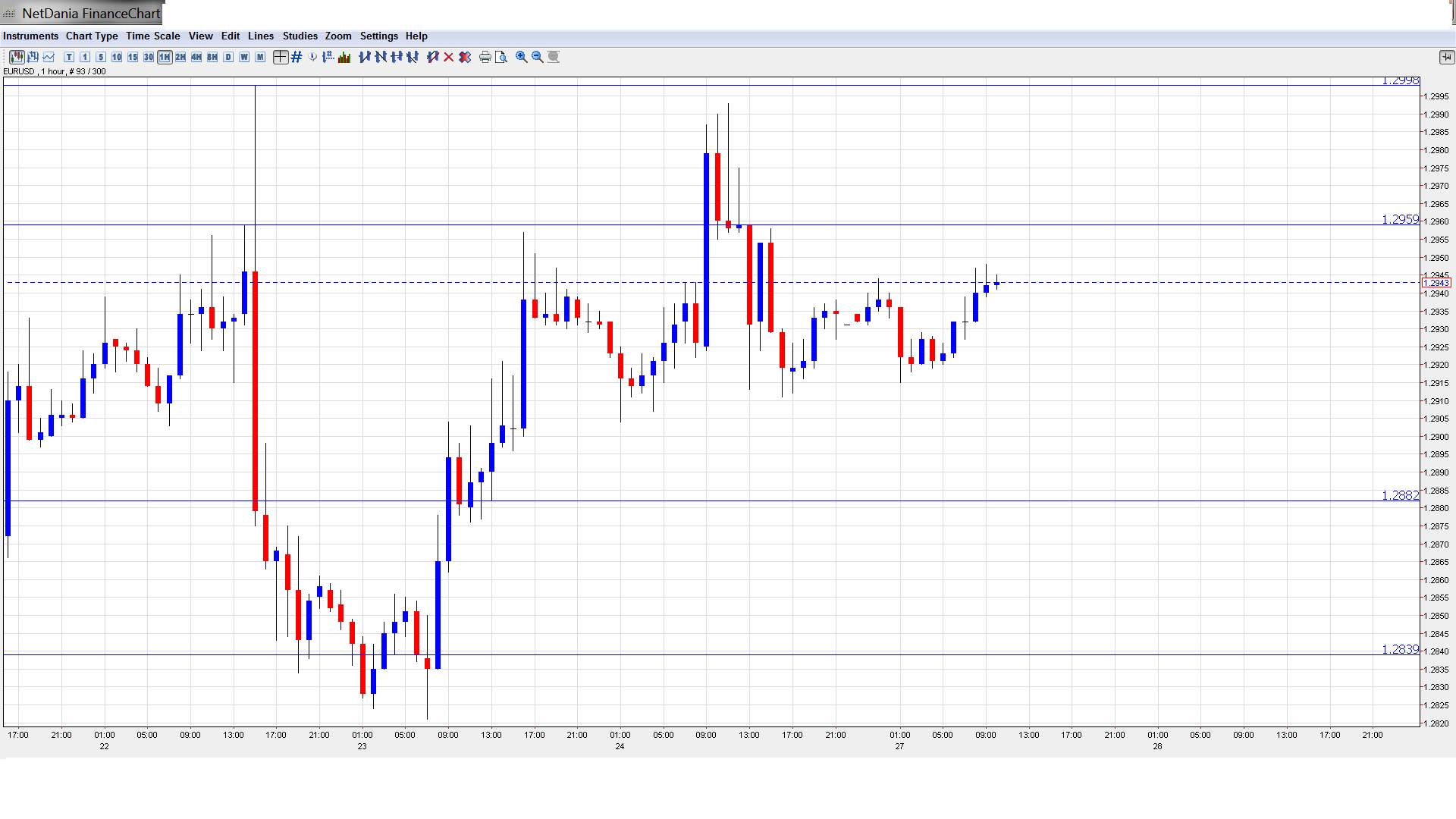

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

EUR/USD Technical

- Asian session: Euro/dollar was steady, as the pair dropped to a low of 1.2915, and consolidated at 1.2938. There is no change in the European session.

Current range: 1.2880 – 1.2960.

Further levels in both directions:

- Below: 1.2890, 1.2840, 1.2800, 1.2750, 1.27, 1.2624 and 1.2587.

- Above: 1.2960, 1.30, 1.3050, 1.31, 1.3160 and 1.32, 1.3255, and 1.3290.

- 1.2880 continues to provide support.

- 1.30 is at strong resistance line.

Euro starts off week quietly in thin holiday trading – click on the graph to enlarge.

EUR/USD Fundamentals

- There are no releases on Monday from the Eurozone or the US.

For more events and lines, see the Euro to dollar forecast

EUR/USD Sentiment

- German numbers rebound: After some lukewarm PMI data out of Germany earlier in the week, there was positive news out of the Eurozone’s number one economy on Friday. GfK German Consumer Climate posted its highest level in almost six years, and IFO Business Climate surprised with a better than expected figure. German GDP bounced back from a decline in Q4, posting a modest 0.1% gain. We’ll get a better picture of the direction of the German economy this week, with the releases of German CPI, Unemployment Change and Retail Sales.

- More positive news from the US: The markets are used to ups and downs in US numbers, and we continue to see alternating weeks in economic data: after a weak Philly number and a jump in jobless claims, last week brought better than expected new home sales, a record low in continuing claims and a nice rise in durable goods orders on Friday. What is the bottom line? The Fed must be wondering the same thing, and has maintained course with the current round of QE.

- Bernanke sends euro on wild ride: US Federal Reserve Chair Bernanke triggered a big drama: He first stated that tightening monetary policy could hurt the economic recovery. The euro reacted by rising sharply, testing the 1.30 level, but this proved to be a short-lived move. Bernanke later said that if US economic data improved, a decision to scale back QE could be taken in the “next few meetings”. This brought the euro back down in a hurry, Hints from Fed officials about whether QE will be maintained will continue to rock the markets.

- Fed split over QE: Overshadowed by Ben Bernanke’s testimony in Congress was the release of the minutes of the most recent FOMC policy meeting. The minutes indicate that the US recovery will have to deepen before the Fed will consider exiting from QE. The policy members were split, as some proposed tapering QE next month, while others were in favor of increasing QE, given the weak inflation readings we are seeing. It should be noted that the minutes relate to a meeting which took place at the beginning of May, in contrast to the fresh testimony of Bernanke on Wednesday.

- Japanese stock market crash: the reaction to the thought of QE tapering was a drop in US stocks, which was followed by a crash in Japan, of 7.32%. This put the Nikkei index in the spotlight. Moves in Japan will likely have an indirect impact on the euro in the weeks to come.