It’s been a rough week for the EUR/USD, but the pair is steady in Friday’s European session, trading in the low 1.28 range. The euro was helped by weak US data on Thursday, as employment and GDP numbers missed expectations. In Cyprus, banks across the country reopened for the first time in almost two weeks, with relative calm reported. In economic news, French Consumer Spending disappointed, as it was way off the estimate. In the US, Friday’s highlight is the UoM Consumer Sentiment.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

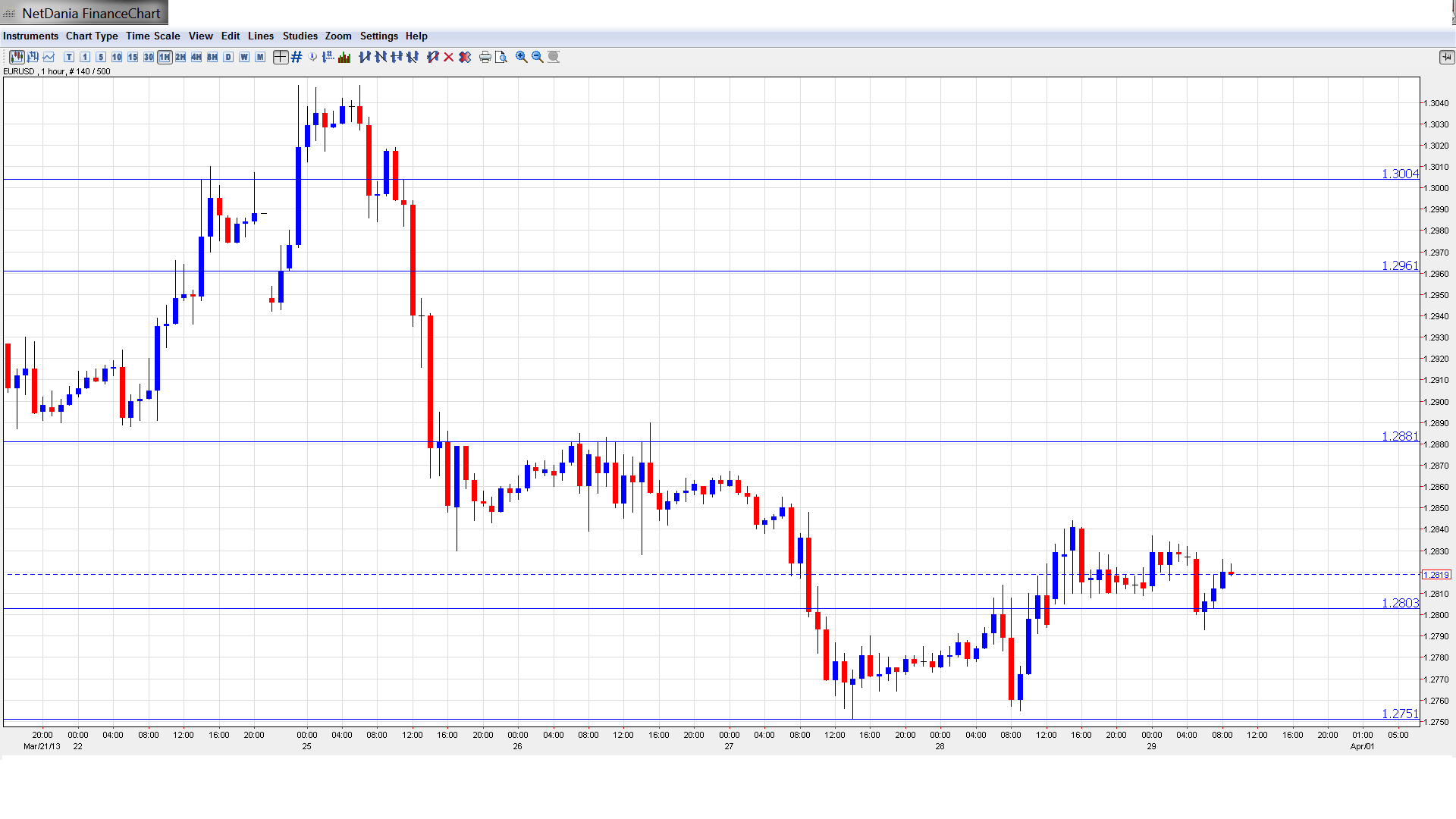

EUR/USD Technical

- Asian session: Euro/dollar dipped below the 1.28 line late in the session. In European trading, the pair has crossed back above 1.28.

- Current range: 1.2805 to 1.2880

Further levels in both directions:

- Below: 1.2805, 1.2746, 1.27, 1.2660 and 1.2587.

- Above: 1.2805, 1.2880, 1.2960, 1.3000, 1.3100, 1.3130 and 1.3170.

- 1.2805 is providing weak support to the pair. 1.2746 is stronger.

- 1.2880 is the next resistance line.

Euro steady as Cyprus concerns recede, US numbers weak– click on the graph to enlarge.

EUR/USD Fundamentals

- 7:45 French Consumer Spending. Exp. 0.3%. Actual -0.2%

- 10:00 Italian Preliminary CPI. Exp. 0.3%

- 12:30 US Core PCE Price Index. Exp. 0.1%

- 12:30 US Personal Spending. Exp. 0.6%

- 12:30 US Personal Income. Exp. 1.0%

- 13:55 US Revised UoM Consumer Sentiment. Exp. 73.2 points

- 13:55 US Revised UoM Inflation Expectations

For more events and lines, see the Euro to dollar forecast

EUR/USD Sentiment

- Cyprus Jitters Ease: The Cyprus bailout crisis, which has been in the financial headlines for the past two weeks, has eased, at least for now. There was calm as country’s banks reopened on Thursday, after being tightly shut for almost two weeks. Fearing a bank run, the government has imposed strict controls, including limiting withdrawals to 300 euros a day, and a ban on cashing checks. Under the bailout agreement between Cyprus, the EU and the IMF, bank deposits under 100,000 euros will continue to be insured. However, it remains unclear what kind of tax will be imposed on larger desposits. As well, under the agreement, Laiki, one of the country’s biggest banks, will be shut down.The original bailout agreement provided for a tax on all Cypriot bank deposits, and this had fueled fears that bank deposits could be taxed or seized in any EU country. Although this tax grab was quickly shelved after a huge outcry in Cyprus, the damage to investor confidence will take time to repair.

- Italian Political Crisis Continues: The markets have been busy with the Cyprus bailout fiasco for the past two weeks, but the crisis in Italy hasn’t magically disappeared, and help does not seem on the way. Coalition talks have not made progress, as the anti-establishment 5-Star Movement has rejected overtures from center-left leader Pier Luigi Bersani. New elections may be the only solution for the Eurozone’s third largest economy. Analysts have noted that Greece also was forced to call new elections, and such a move will certainly not increase investor confidence in the Eurozone.

- Which way Germany?: Mario Draghi is exuding confidence that the Eurozone economy will improve later in 2013, but that certainly won’t happen if the German economy doesn’t lead the way. However, German data has been a mix recently, and this was underscored in Thursday’s releases. Retail Sales rose 0.5%, blowing past the estimate of a 0.4% decline. However, Unemployment Change hit a five-month high, jumping to 13 thousand. This was a major disappointment, as the markets had anticipated a respectable drop of 2 thousand. Unemployment was unchanged at 6.9%.

- US data disappoints: There has been a lot of talk of the US recovery gaining traction, but this week has been a bust, as economic releases pointed to weakness in a wide range of sectors in the US economy. There were two major housing releases this weeks, and hopes of strong numbers were dashed. New Home Sales fell sharply from 437 thousand to 411 thousand, well below expectations. Pending Home Sales, also looked weak, declining 0.4%. The forecast stood at -0.3%. Unemployment Claims have looked sharp over the past four weeks, but slumped this time around, coming in at 357 thousand, well above the estimate of 340 thousand. Final GDP rose 0.4%, missing the forecast of 0.5%. Earlier in the week, manufacturing and consumer confidence also missed their estimates. Put simply, this has been a week has been one that the markets will be happy to forget.

0 comments :

Post a Comment