Eur/USD remains under pressure, and is struggling to remain above the 1.30 line in Tuesday’s European session. It is another quiet day as far as economic releases. In the Eurozone, today’s only releases are German inflation figures. Final CPI came in as expected, but WPI fell below the estimate. In the US, today’s highlight is the Federal Budget Balance, and the markets are bracing for a large deficit for the March release.

Eur/USD remains under pressure, and is struggling to remain above the 1.30 line in Tuesday’s European session. It is another quiet day as far as economic releases. In the Eurozone, today’s only releases are German inflation figures. Final CPI came in as expected, but WPI fell below the estimate. In the US, today’s highlight is the Federal Budget Balance, and the markets are bracing for a large deficit for the March release.

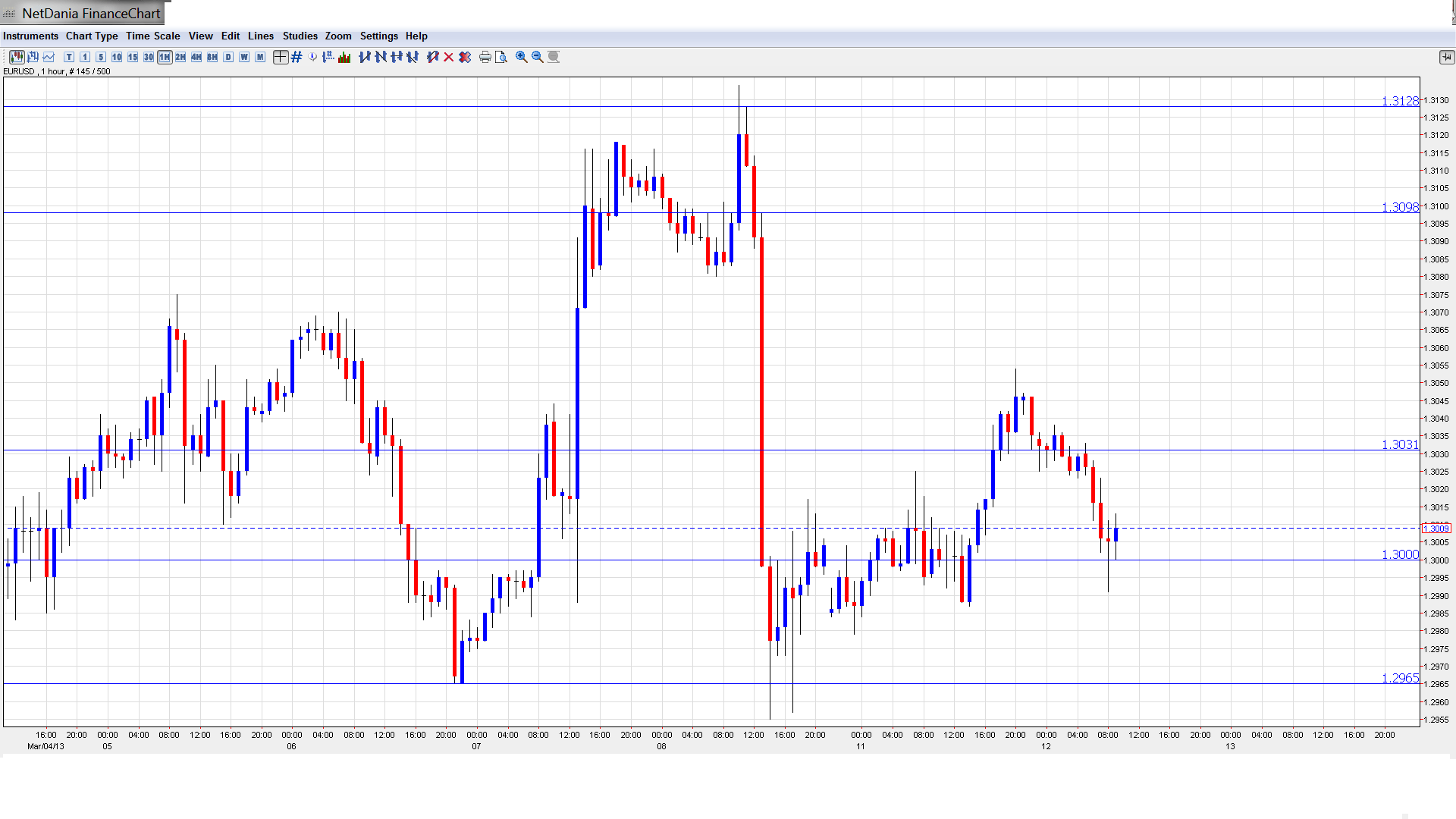

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

EUR/USD Technical

- Asian session: Euro/dollar edged lower, touching a low of 1.3012. The pair consolidated at 1.3016. In the European session, the pair has dipped just under the 1.30 level.

- Current range: 1.2960 to 1.3000.

- Further levels in both directions:

- Below: 1.2960, 1.2880, 1.2805, 1.2746, 1.27, 1.2660 and 1.2587.

- Above: 1.3000, 1.3030, 1.3100, 1.3130, 1.3170, 1.3255, 1.3290, 1.3350, 1.34, 1.3486 and 1.3588.

- The pair is testing 1.30 on the upside. 1.3170 remains a key line of resistance.

- 1.2960 is the next support level. 1.2880 is stronger.

Euro/dollar continues to test the 1.30 line – click on the graph to enlarge.EUR/USD Fundamentals- 7:00 German Final CPI. Exp. 0.6%. Actual 0.6%

- 7:00 German WPI. Exp. 0.4%. Actual 0.1%

- 11:30 US NFIB Small Business Index. Exp. 91.3 points

- 18:00 US Federal Budget Balance. Exp. -200.0B

For more events and lines, see the Euro to dollar forecastEUR/USD Sentiment- Euro goes for a ride: The euro took traders for a roller coaster ride last Thursday and Friday. The continental currency shot up after the ECB maintained interest rates at 0.75%, and gained over one cent against the US dollar. On Friday, the euro coughed up almost all of those gains, closing the week just under the 1.30 level. The catalyst for the sharp drop was outstanding US employment numbers, which gave a boost to the dollar. As well, the euro was hurt by German Industrial Production, which came in at a flat 0.0%, well below the market estimate. The euro has quieted down this week, as it trades very close to the 1.30 level.

- US employment numbers shine: US employment indicators looked very sharp last week. Unemployment Claims dropped to 340K, well below the estimate of 354K. Non-Farm Employment Claims hit 236 thousand, smashing past the forecast of 162 thousand. The Unemployment rate fell nicely, dropping to 7.7% from 7.9%. Has the US recovery entered a new phase? The strong figures helped the dollar post sharp gains against the euro at the end of the week, and we could see the greenback make further gains if US number numbers continue to shine.

- Fitch downgrades Italy, Spain: On Friday, Fitch Ratings downgraded the debts of Italy and Spain, as well as Belgium, Cyprus, and Slovenia. All these countries are members of the Eurozone, and Fitch warned that European leaders were not acting decisively enough to combat the debt crisis affecting the continent. Markets pay close attention to such downgrades, as countries with lower ratings generally are forced to pay more to borrow funds. Italy was lowered to a rating of -A, and Spain was lowered to A. Fitch also placed a negative outlook on all five members, meaning that there is greater than 50 percent chance of another downgrade in the next two years. The downgrade is likely to exacerbate Italy’s severe political and economic problems. The country is embroiled in a political crisis, and is struggling to contain a massive debt of 1.9 trillion euros.

- Fed may revisit QE: The US has posted some solid economic releases lately. Last week saw employment numbers go way up and the Unemployment Rate drop to 7.7%, its lowest level since 2008. The improving economy has led to speculation that the Fed might wind up its current round of QE, which involves the purchase of $85 billion in assets each month, earlier than expected. Federal Reserve officials are now mulling over the possibility of allowing the trillions of dollars in securities they have purchased to mature, rather than drowning the market with huge sales of securities. The economy continues to recover slowly, and has had a lukewarm response to the Fed’s massive purchase of assets. This “new exit” strategy could take place as early as June, and would be a dramatic shift in the Fed’s current monetary policy.

0 comments :

Post a Comment